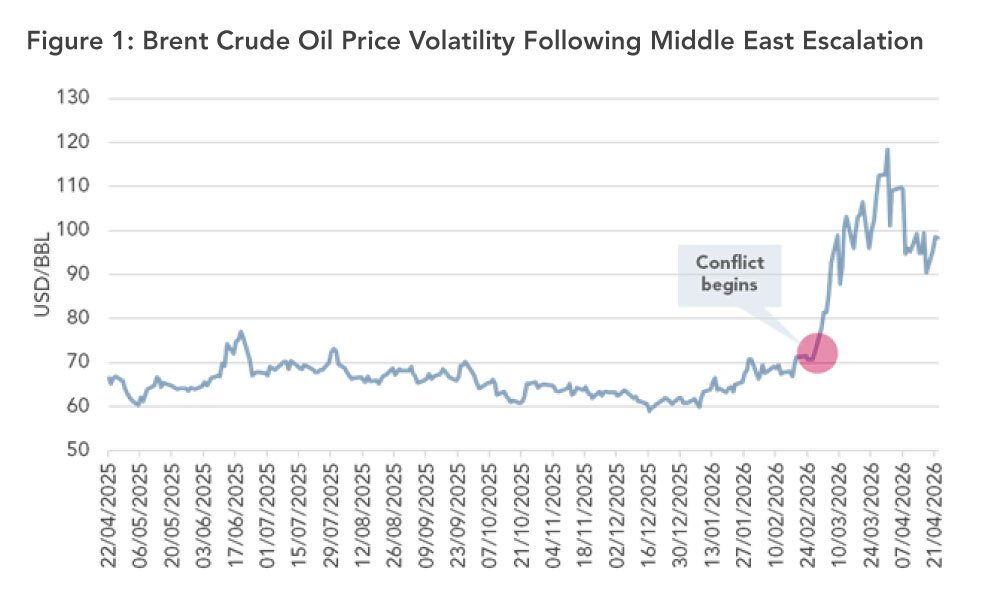

Escalating tensions involving Iran are driving renewed volatility in global energy markets, with direct implications for construction.

Oil and gas prices have risen and remain highly sensitive to disruption, particularly given the strategic importance of the Strait of Hormuz to global energy supply.

Key transmission routes to construction:

- Energy-related increases in manufacturing costs

- Higher fuel and logistics costs

- Supply chain disruption and rising insurance risk

- Targeted pressure on energy-intensive materials

Early indicators suggest these factors are beginning to influence pricing and procurement behaviour.

Key message: This is best understood as a volatility and pricing risk shock, rather than a repeat of the 2022 inflation cycle but conditions remain highly sensitive to further escalation.

ENERGY MARKETS – PRIMARY TRANSMISSION CHANNEL

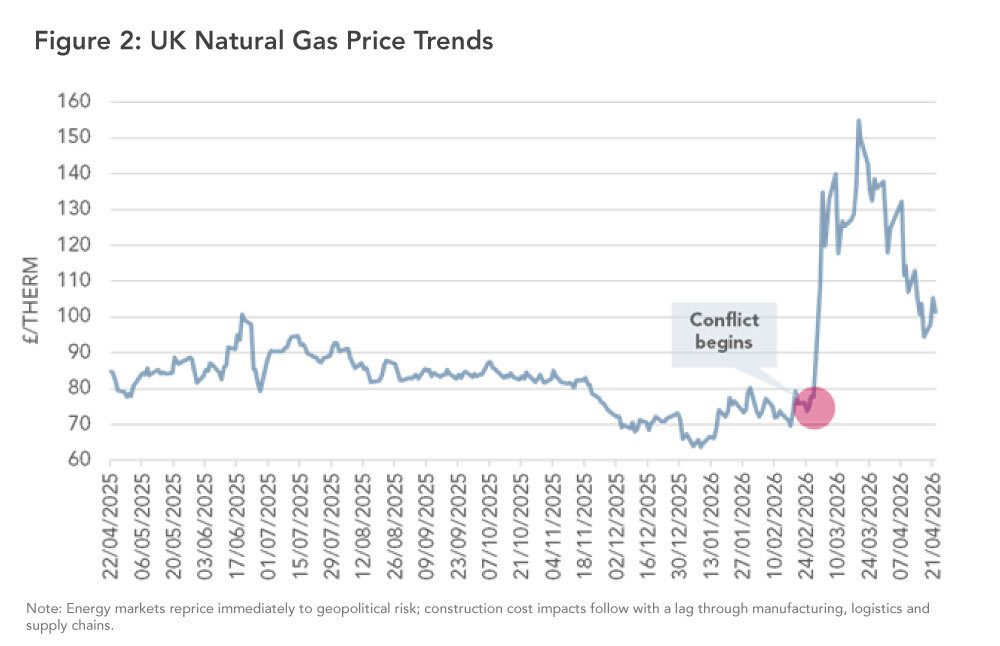

Energy markets have reacted rapidly to geopolitical developments, with oil and gas prices rising sharply before partially easing.

- Price movements have been driven primarily by disruption risk and constrained flows rather than a sustained loss of supply

- Energy markets reprice immediately, while construction impacts emerge with a lag

- Cost impacts feed through via manufacturing, transport and logistics rather than direct material shortages

In practical terms, this means construction cost impacts are delayed, partial and uneven, rather than immediate or universal.

EARLY MARKET SIGNALS

Initial feedback from contractors and suppliers indicates that market behaviour is beginning to shift.

Key observations include:

- Selective cost pressure emerging in fuel-sensitive and energy-intensive inputs

- Reduced willingness to hold fixed prices

- Shorter quotation validity periods

- Increased scrutiny of supply chain exposure

These signals typically emerge early in the cycle and often precede broader cost movement, suggesting that upstream pressures are beginning to transmit into construction markets, albeit unevenly.

LESSONS FROM RECENT ENERGY SHOCKS (UKRAINE BENCHMARK)

The Russia–Ukraine conflict provides a useful benchmark for how geopolitical shocks transmit into construction markets. However, the current environment differs in several important respects.

Key similarity

- Energy remains the primary transmission mechanism into construction costs

Key differences

- No direct structural disruption to core construction material supply

- Effects are indirect and energy-led rather than supply-constrained

- Energy disruption, to date, appears more volatile than structural, with no sustained or structural loss of supply comparable to 2022

A further distinction is that the industry is now better prepared, with more cautious pricing strategies and improved energy risk management following the previous crisis.

Implication

The current environment is more likely to result in selective cost pressure, procurement friction and tighter risk management, rather than universal price escalation.

EARLY MARKET RESPONSE

Feedback from live projects suggests a market that is becoming more cautious but remains operational.

Common themes include:

- Supply chains largely holding where procurement is already secured

- Increased focus on imported and specialist components

- Early pricing signals emerging across selected materials and packages

The clearest pressure points are in:

- Steelwork and façades

- MEP and specialist systems

- Energy-intensive and imported materials

Overall, the market is not experiencing systemic disruption, but is increasingly:

- Stress-testing supply chains

- Adjusting procurement strategies

- Repositioning pricing and risk

This reflects a shift in behaviour ahead of confirmed impacts, with contractors increasingly managing exposure to potential volatility rather than responding to realised disruption.

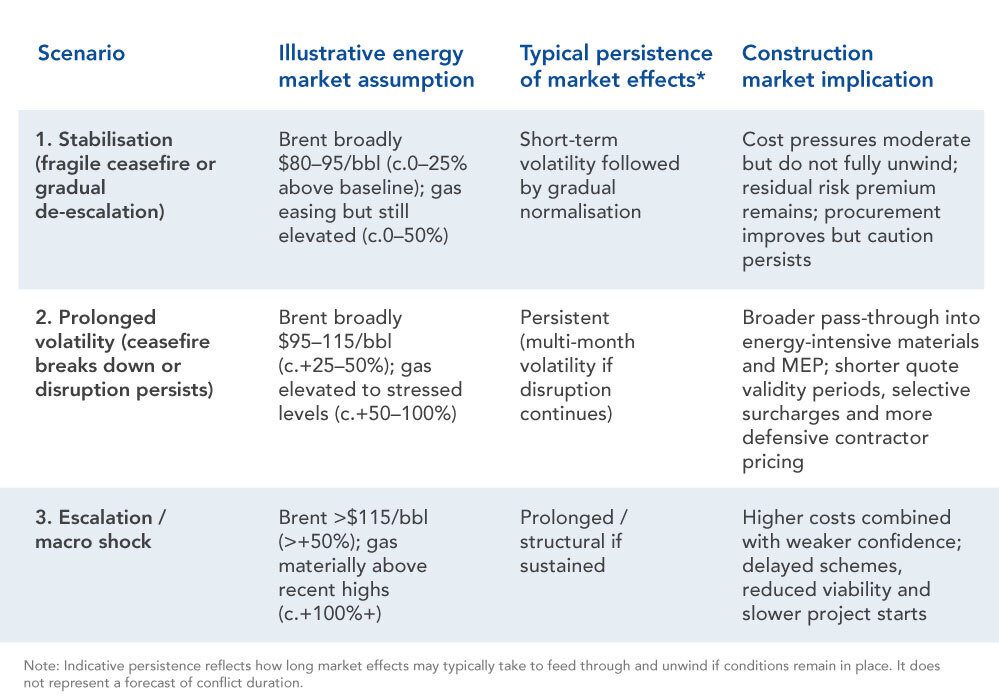

SCENARIO FRAMEWORK

The outlook for construction will depend on whether disruption to energy markets and supply chains proves temporary or persistent.

At present, conditions are broadly consistent with a stabilisation scenario, although the margin for stability remains narrow.

This framework highlights how volatility in energy markets may transmit into construction under different conditions. Outcomes will vary depending on the duration and severity of disruption, supplier pricing behaviour and prevailing market dynamics, and should be interpreted as directional rather than predictive.

Impacts will also vary by project, reflecting differences in procurement timing, supply chain exposure and project characteristics, as well as overlapping influences from oil, gas and logistics cost drivers.

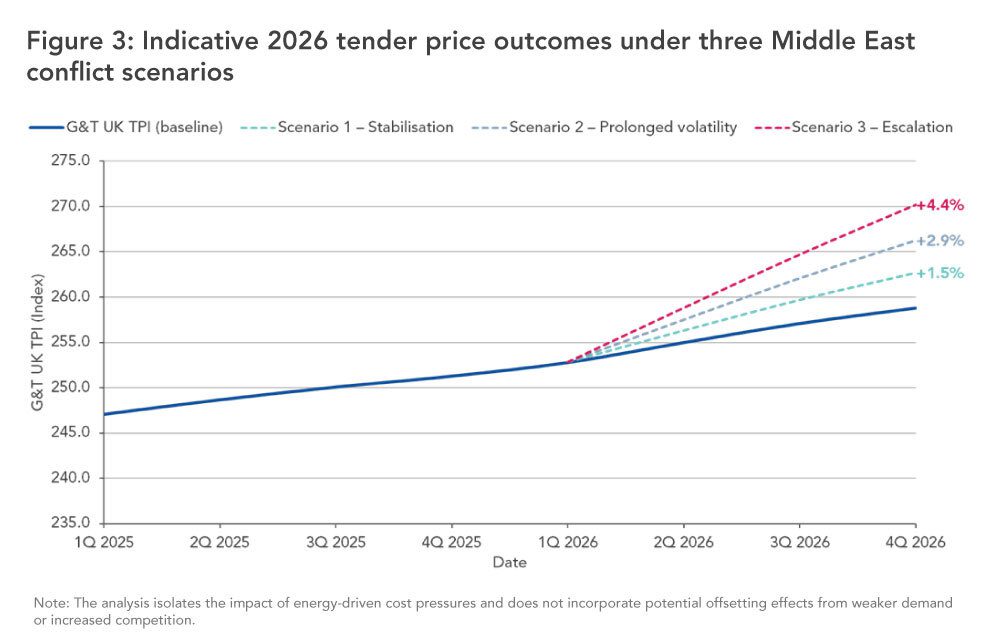

The chart below illustrates a range of potential tender price outcomes in 2026 under three Middle East conflict scenarios, shown relative to the current G&T TPI baseline.

The scenario lines represent the upper bound of potential outcomes, assuming a high degree of cost pass-through from energy and input price shocks over the course of 2026. They are intended to demonstrate the possible scale of impact, rather than a central forecast.

In practice, the extent and timing of pass-through will depend on market conditions, procurement dynamics and contractor behaviour — including levels of competition, risk appetite and pipeline visibility. As such, these scenarios should be interpreted as illustrative sensitivities, not predictions.

For simplicity, the model assumes that the impact is realised within 2026. In reality, cost pass-through is typically partial and lagged, and may extend beyond 2026 depending on contract structures, pricing mechanisms and supply chain dynamics.

Actual tender price outcomes may therefore be lower, delayed, or more muted if market conditions constrain the ability to fully recover cost increases.

IMPLICATIONS FOR CLIENTS

The immediate implication is not that projects should pause, but that responses should become more selective and risk-aware.

Key considerations include:

- Continued progression for schemes with strong fundamentals

- Greater focus on procurement timing and supply chain engagement

- Increased sensitivity to pricing volatility and quotation validity

- More targeted approach to contingency and risk allocation

Public and infrastructure sectors are likely to remain more resilient than more commercially sensitive private-sector development.

CONCLUSION

The Middle East conflict introduces a clear source of volatility into construction markets, primarily through energy and supply chain channels.

Current evidence points to:

- Selective cost pressure rather than systemic inflation

- A need to manage procurement and pricing risks even more diligently

- A more fragile but still functioning market environment

While risks remain elevated, most projects should be able to progress, provided procurement strategies reflect current market conditions and supply chain dynamics.

If you have any questions or would like to discuss the potential implications for specific projects, please contact Michael Urie or your main G&T contact.